Constellation Software: A Generational Opportunity The Market Is Missing

Why AI fears and acquisition worries may be causing investors to underestimate one of the best compounders in public markets.

TL;DR

Constellation Software has been one of the best compounders in public markets for decades, but the stock now trades at a noticeably lower multiple than it usually has. A lot of that seems tied to broad AI fears and worries that the company might struggle to keep finding enough acquisitions as it gets bigger. Mark Leonard’s departure is another worry.

But many of Constellation’s businesses aren’t typical software products. They’re deeply embedded vertical systems that organizations rely on to actually run their operations. In other words, they behave more like infrastructure than optional tools. If those dynamics hold up (and if management can keep reinvesting cash at decent returns) today’s valuation may already be pricing in more pessimism than the business really deserves.

I Wanted To Get This Article Out Earlier, But CSU Is Still Attractive After The Bounce

Before going further, it’s worth acknowledging the timing of this article.

I actually wanted to publish this deep dive earlier, but it took longer to finish than expected. I’ve been mentioning Constellation Software in my weekly watchlists for some time now. About a month ago, I highlighted the stock after the big sell-off, noting that the underlying business still looked healthy despite the AI panic hitting software stocks. Then, about five days ago, I mentioned it again as the chart started showing signs of stabilization.

Since then the stock has already moved quite a bit, climbing from a low of ~$2,200 to around $2,900+. That kind of move naturally makes investors wonder whether the opportunity has already passed. But I say no.

At the same time, the timing is still interesting because the company reports earnings on March 9 before the market opens. That report should give investors another data point on whether the compounding engine is still running the way it has for decades.

Either way, the bigger question remains the same: is the market suddenly underestimating one of the most consistent compounders in public markets?

One of the Best Compounders in the World

For a long time, Constellation Software looked like it had cracked a formula that almost nobody else in software could replicate.

The idea sounded simple enough: buy small niche software companies, keep them forever, collect the cash they generate, and use that cash to buy more niche software companies. Then repeat that process over and over again for decades. The concept itself wasn’t revolutionary. What made it special was the discipline required to execute it consistently across 600+ software acquisitions over the years.

Over time that approach turned Constellation into one of the most efficient acquisition machines in the software industry. Instead of chasing hype cycles or trying to build the next big platform, management focused on acquiring profitable niche businesses and reinvesting their cash flows into the next opportunity. Each acquisition added more recurring revenue and more cash flow that could be redeployed into future deals. Eventually the process started feeding itself.

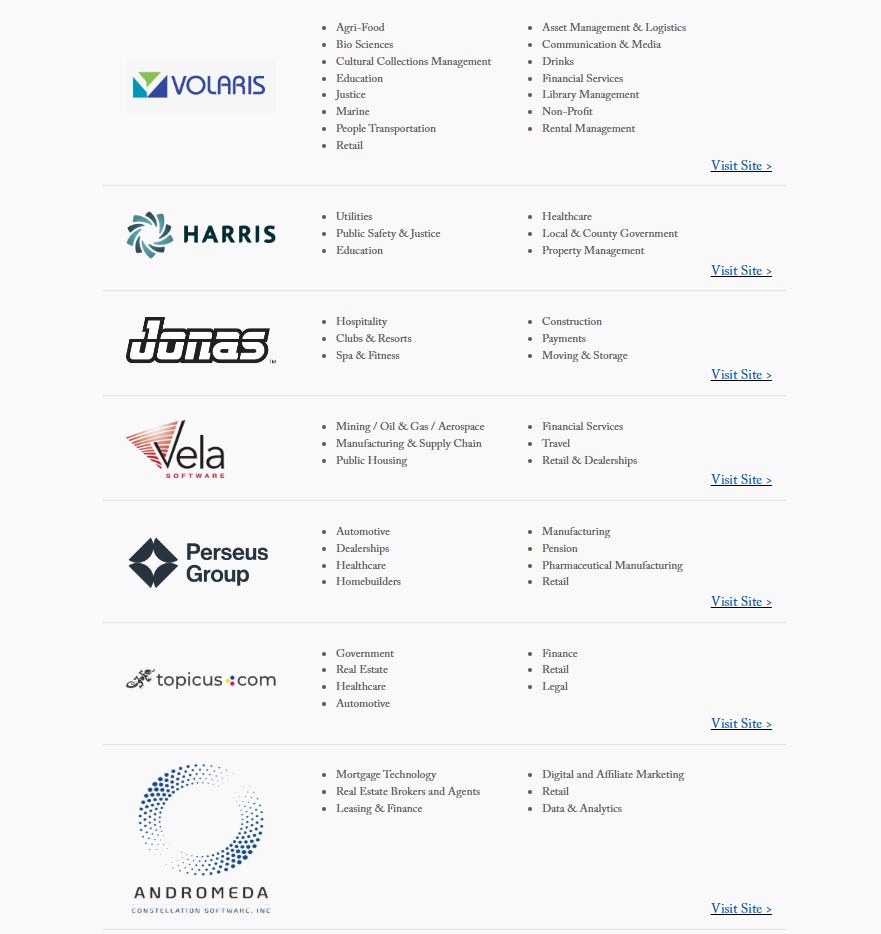

Today, the company operates through several decentralized operating groups. It owns the companies below (Volaris, Harris, etc.) and these companies themselves own several companies and do their own acquisitions in their own niches.

You can think of these operating groups almost like mini-Constellations inside the larger company. Topicus.com (TOI.V), listed below, is also its own stock that Constellation Software spun off a few years ago, but that’s a topic for a different day.

The company’s strategy hasn’t changed over the years: find small, durable software businesses, buy them at reasonable prices, keep them permanently, and reinvest the cash they generate. Over decades, that approach has produced one of the most remarkable compounding stories in the public markets.

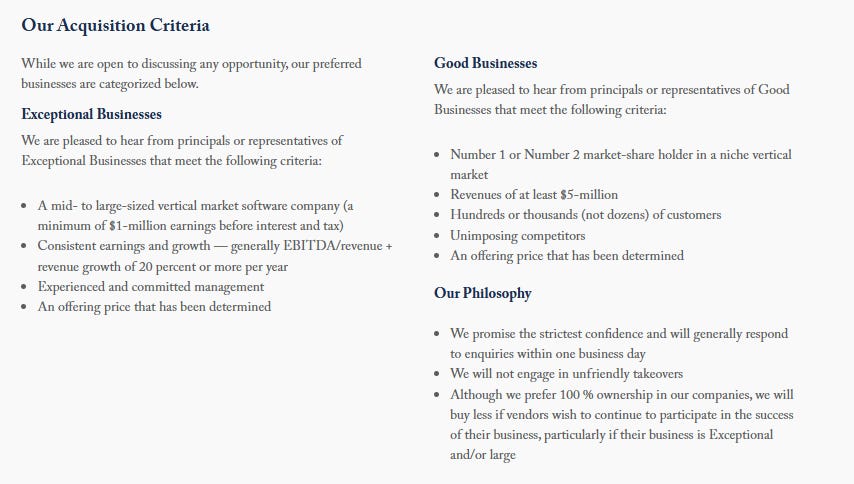

The company even lays out its acquisition criteria plainly on its site. It’s not even a secret formula. You can see it below.

But that’s what makes the current moment interesting. For the first time in a while, the market doesn’t seem quite as confident that this company will be fine in the long term.

Why The Stock Is Suddenly Viewed Differently

Constellation used to trade with almost automatic optimism. Investors believed the company could keep finding attractive acquisitions and reinvesting capital at high returns for decades. Because of that belief, the stock often traded at a very rich multiple.

That confidence has cooled down quite a bit. The valuation has come down a lot, and the conversation around the company has shifted. Investors are now asking questions that used to get brushed aside.

Could AI lower barriers to entry in software and make some of Constellation’s businesses easier to compete with? Can the company really keep finding enough acquisition targets now that it has become so large? And with Mark Leonard (legendary founder) no longer the President of the company due to health reasons (he’ll still be Director on the Board), does the next chapter of the company look different from the last one?

Those are all fair questions. In fact, they’re the right questions. But I also think the market may be approaching them from the wrong starting point. The market has treated Constellation like a typical software company at exactly the moment when the most important thing about it is that it isn’t a typical software company.

Understanding that difference is key.

What Constellation Actually Owns

When most investors hear the word “software,” they picture big horizontal platforms competing across massive markets. They think about productivity apps, enterprise cloud systems, flashy demos, and giant total-addressable-market slides.

Constellation lives in a completely different part of the software world.

The company focuses almost entirely on vertical market software, which basically means software built for very specific industries with very specific operational needs. These systems are often used by customers like municipal governments, transit agencies, hospitals, mortgage processors, school districts, and a long list of other specialized organizations.

At first glance, these businesses can look unimpressive. The markets are small. The products aren’t flashy. The customer base can be narrow. But those exact characteristics are often what make them attractive.

In many cases the software becomes deeply embedded in how the customer actually operates. Employees learn the system inside out. Years of historical data accumulate inside it. Other software tools become connected to it. Internal processes slowly evolve around it. Once that happens, the software stops behaving like a normal product and starts behaving more like infrastructure.

Constellation doesn’t win because its software is the most exciting. It wins because its software is often the hardest to rip out.

Running Constellation Through My Compounder Checklist

In a recent article, I outlined a simple checklist I use when evaluating potential long-term compounders. It’s not meant to be a rigid formula, but it helps you weed out the stocks that aren’t worth your money.

So, let’s run it through the checklist, which I’ll expand on later.

Competitive advantage.

Constellation’s moat largely comes from switching costs. As stated earlier, many of its vertical software systems become deeply embedded in the daily operations of organizations like municipalities, transit agencies, hospitals, and school systems, making them difficult and risky to replace.Consistent growth.

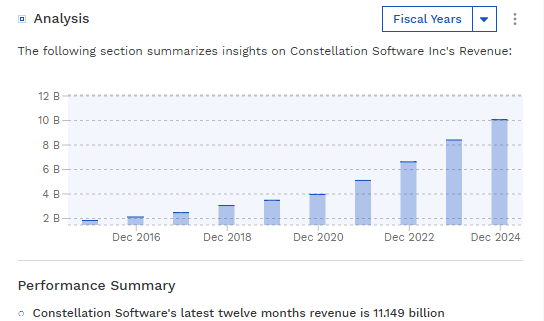

Revenue and cash flow have grown steadily for years as the company repeatedly acquires niche software businesses and reinvests their cash flows into additional acquisitions. Its revenue has grown at over 20% annually for the past 10 years.

Per-share growth.

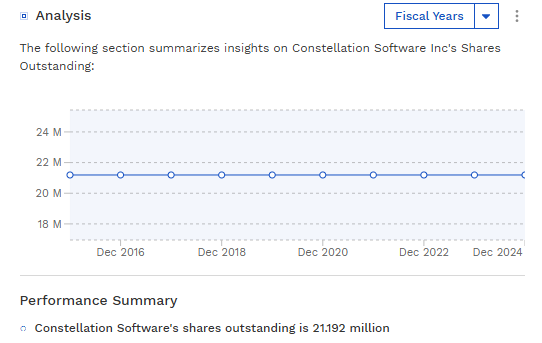

The share count has stayed steady over the years, meaning all its growth translates to per-share growth. No shareholder dilution.

Stable estimates.

Revenue tends to be fairly steady and predictable compared with a lot of other software companies.Reinvestment runway.

There are still thousands of small vertical software companies around the world, so the acquisition pipeline is likely still deep. The real question is whether Constellation can keep finding enough deals as it gets bigger.Debt.

Constellation does use debt to help fund acquisitions, but the businesses it buys usually generate steady recurring cash flow, which helps support that leverage.Secular tailwinds.

Many industries are still moving toward specialized software to run their operations, which should continue supporting demand for the kinds of niche systems Constellation owns.AI positioning.

AI could make it easier to build software, but many of Constellation’s systems are deeply tied into how organizations actually operate, which may make them harder to replace than typical SaaS tools.Valuation.

The stock now trades at a lower multiple of FCFA2S than it has for much of the past decade, suggesting investors are already pricing in some slower growth.Chart analysis.

After a massive long-term run, the stock has panic dipped recently, making it a long-term buy.

Ultimately, running Constellation through this checklist highlights the key question for investors: can the company continue reinvesting capital at attractive returns as it grows larger? I’ll talk about that later on, but for now, it’s important to talk about FCFA2S, the most important metric for CSU.

FCFA2S: The Metric Serious CSU Investors Watch

If you want to understand how Constellation creates value, it also helps to focus on the right metric.

A lot of investors casually look at regular free cash flow when evaluating the company. But long-time Constellation followers often focus on a more conservative metric called Free Cash Flow Available to Shareholders, or FCFA2S. The idea behind FCFA2S is to capture the cash that truly belongs to shareholders after accounting for things like minority interests and other claims on the company’s earnings.

In other words, it’s meant to be a more honest version of free cash flow.

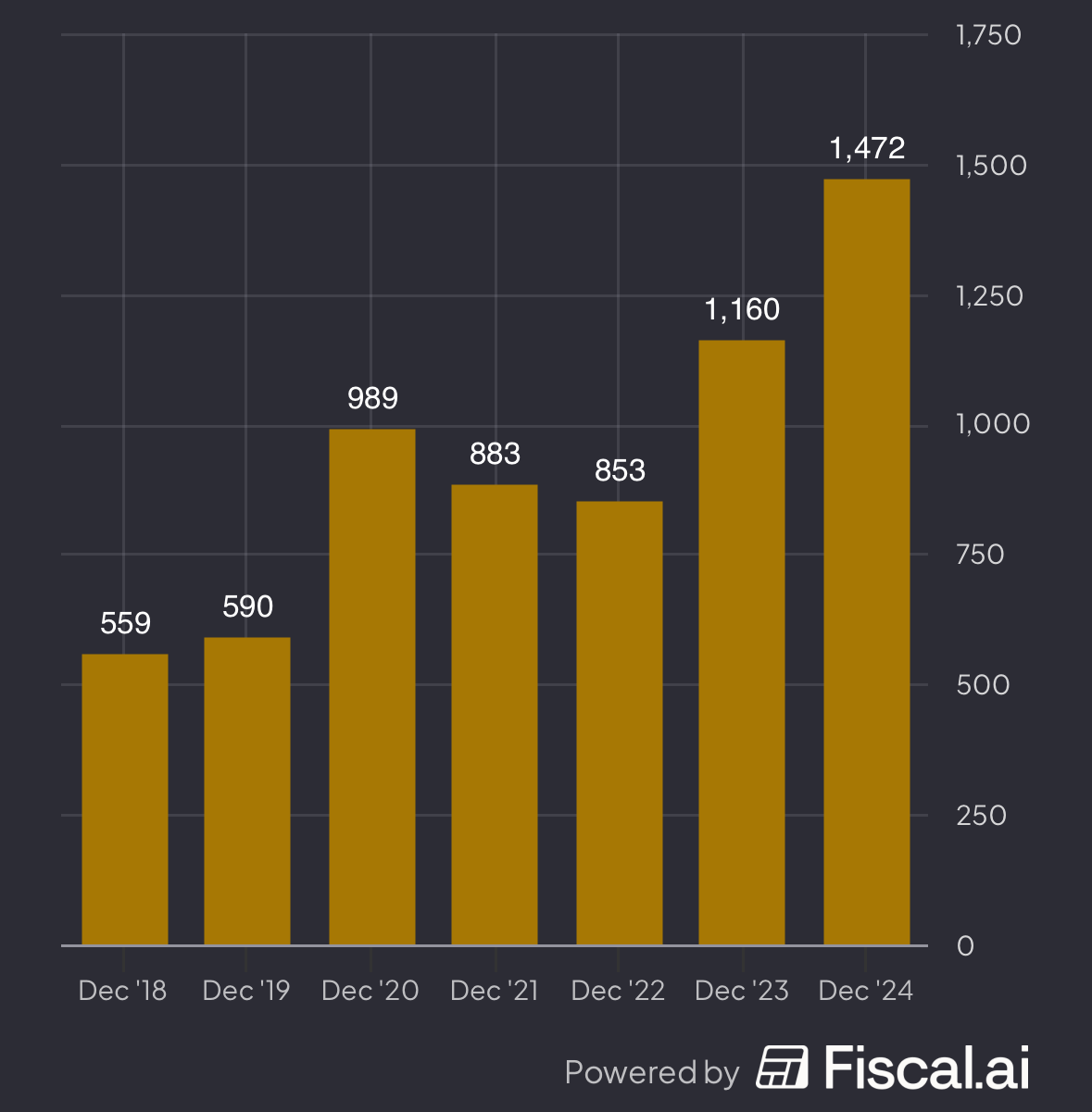

And by that measure the growth has been extremely impressive. FCFA2S was about $559 million in 2018. It rose to roughly $590 million in 2019, then jumped to around $989 million in 2020. After that it came in near $883 million in 2021, about $853 million in 2022, roughly $1.16 billion in 2023, and approximately $1.47 billion in 2024. Using a trailing twelve-month estimate based on recent results, the number now sits around $1.74 billion. The growth over this time frame was 163.3%, or a 17.5% CAGR.

It’s also worth noting that Constellation has spun off parts of its business over time. In 2021, its European operations became Topicus (TOI.V) stock, and in 2023 its communications software portfolio became Lumine Group (LMN.V) stock. Those businesses used to be fully included in Constellation’s cash flow numbers, but today they operate as independent public companies. That means Constellation’s reported FCFA2S now reflects only the cash flow from the remaining portfolio, even though the broader ecosystem of companies that originated inside Constellation continues generating additional cash in separate entities.

Anyway, this isn’t the profile of a company living off promises or hype cycles. It’s the profile of a business that has repeatedly turned acquisitions into real shareholder cash flow.

What Investors Have Historically Paid for Constellation

Because Constellation’s business model has been so successful, the market has historically been willing to pay a premium valuation for the company. Looking at historical data, the stock has often traded at very high multiples of FCFA2S.

For example, around early 2019 the company had a market capitalization of roughly $18 billion USD while generating about $559 million in FCFA2S. That implied a valuation of roughly 32x FCFA2S. The following year the multiple remained in a similar range. In 2021 the company’s market cap had grown to around $29.6 billion, and even then the valuation still hovered around 30x FCFA2S.

During more optimistic periods, the valuation climbed even higher. By 2023 and 2024 the company briefly traded at multiples approaching 45 to 50x FCFA2S as investor enthusiasm reached extreme levels. Even during market corrections, the valuation rarely dropped below roughly 30x FCFA2S.

Today, using a market cap of roughly $43.36 billion and trailing FCFA2S of approximately $1.74 billion, the company trades at roughly 26 times FCFA2S. After it reports earnings on March 9, that figure will probably drop to 25x if FCFA2S improves year-over-year. That’s noticeably lower than the valuation range investors have historically assigned to the business.

In other words, the market is currently pricing Constellation more conservatively than it has for most of the past several years, suggesting that investors are already discounting many of the concerns surrounding the company. AI fears, slower acquisition growth, and leadership transitions are all reflected in the current price.

A Simpler Way To Think About The Valuation

Another way to look at Constellation is to ignore fancy valuation models and ask a much simpler question: what happens if the business just keeps compounding?

Right now the stock trades at roughly 25× FCFA2S based on my estimates after the upcoming earnings report. Historically the multiple has often been higher, but instead of assuming any multiple expansion, it’s safer to assume the opposite — that the valuation simply stays where it is.

If the multiple stays around 25× and the company grows FCFA2S at roughly 15%+ per year, then over long periods the stock price should grow at roughly the same rate.

That’s because if the underlying cash flow increases by 15% and investors continue valuing the business at the same multiple, the market value should increase at roughly the same pace as the cash generation.

So the real question isn’t whether the multiple expands. It’s whether Constellation can continue growing its cash flow at a healthy rate.

Historically, FCFA2S has grown at roughly 17–18% annually over the past several years. That doesn’t mean the same pace will continue forever — the company is much larger today, and sustaining that level of growth becomes harder as the capital base expands.

But even if growth slows somewhat, something like mid-teens compounding could still produce very attractive long-term returns if management continues allocating capital intelligently.

In other words, this investment thesis doesn’t depend on the market suddenly getting excited about the stock again. It mostly depends on the underlying compounding machine continuing to do what it has done for decades.

And so far, that machine still appears to be running.

The AI Bear Case Is Too Simplistic

A lot of the current concern around software comes from the idea that AI will make it dramatically easier to build competing products. If software becomes easier and cheaper to create, the thinking goes, then barriers to entry could fall and competition could increase.

There’s some truth to that.

But the argument starts to break down when you apply it to vertical market software that’s already deeply embedded inside a customer’s operations. In those situations the real moat often has less to do with the code itself and more to do with everything built around it.

The real moat in many Constellation businesses isn’t the software. It’s the operational mess a customer would create by trying to replace it.

And you can see that clearly when you imagine what switching actually looks like in the real world.

What Happens If Someone Actually Tries to Replace the Software

To understand why many of Constellation’s businesses are harder to disrupt than they appear, it helps to look at what would actually happen if a customer tried to replace one.

Take Trapeze Group, one of the companies in Constellation’s portfolio (within Volaris Group). Trapeze builds software used by transit agencies around the world to run bus and rail networks. Its systems handle things like route planning, driver scheduling, dispatch coordination, vehicle tracking, and maintenance management. In many cities, the software essentially acts as the operational brain of the transit system.

Now imagine a realistic scenario.

A mid-size city transit authority has been using Trapeze’s software for over a decade. During that time the system has become deeply integrated into the agency’s operations. Dispatchers rely on it every day to assign drivers and manage routes. Maintenance teams use it to track vehicle repairs. Ridership data from ticketing systems flows into it. Payroll calculations depend on it for overtime rules. Over the years, thousands of operational decisions have been built around the logic inside the system.

Then one day a startup shows up with a pitch.

They claim they’ve built an AI-powered transit platform that can optimize routes in real time, predict delays, and improve efficiency. The demo looks slick. The interface is modern. Compared with the older system the agency has been using, the new platform looks like a clear technological upgrade.

After several meetings, the transit authority decides to try it.

The vendor promises that migrating away from the existing system will take only a few months. The agency approves the project and begins planning the transition.

But almost immediately things start getting complicated.

The first issue is data. The Trapeze system contains years of route schedules, driver assignments, maintenance logs, and historical ridership patterns. None of that data transfers cleanly into the new platform. The formats are different. Some fields don’t match. Some rules for scheduling logic behave differently. Engineers spend weeks writing scripts just to move the data over.

Then the staff training begins. Dispatchers who have been using the old system for years now need to learn a completely new interface. Small mistakes start happening. Drivers receive incorrect shift assignments. Routes are scheduled with unrealistic turnaround times. Dispatchers start manually correcting problems that the old system used to handle automatically.

Next come the integrations.

It turns out the scheduling system is connected to far more systems than anyone remembered. The ticketing platform pulls data from it. GPS vehicle tracking feeds into it. Payroll systems rely on it for overtime calculations. Each of those integrations now needs to be rebuilt.

The timeline begins slipping.

Months pass, and the agency finds itself running two systems at once. The old Trapeze system continues to manage daily operations while the new AI platform struggles to reach full functionality.

Then something breaks.

During a limited rollout, the new platform produces incorrect schedules for several routes. A handful of buses arrive late. Drivers report confusion about shift assignments. Commuters begin filing complaints about service disruptions.

At that point the leadership team faces a difficult decision.

Continue pushing forward with the migration and risk further operational problems, or abandon the project and stick with the system that has been working reliably for years.

In many real-world cases, organizations make the same choice. They revert back to the existing system.

The new AI software may have been impressive in theory, but the operational risk of replacing infrastructure that already works turned out to be far greater than expected.

This is the dynamic that defines much of Constellation’s portfolio. Once vertical market software becomes embedded inside an organization’s workflows, it stops behaving like ordinary software. It becomes infrastructure.

And infrastructure is notoriously difficult to replace.

However, it’s still worth noting that it doesn’t mean these systems are completely immune to competition. Replacements do happen. They usually just happen under very specific circumstances. Sometimes it’s a new leadership team that wants to modernize everything. Sometimes a major contract comes up for rebid. Sometimes regulators force changes. And sometimes the incumbent vendor simply stops investing in the product and lets it deteriorate.

In other words, switching costs don’t eliminate competition entirely. They just raise the bar much higher for anyone trying to replace the existing system. A new product doesn’t just have to be better — it usually has to be a lot better to justify the operational disruption of switching.

The Bigger Risk: Scale

While AI gets most of the attention, the bigger long-term risk for Constellation may simply be scale. The company’s strategy works best in fragmented markets full of small vertical software businesses. As Constellation gets larger, it needs to deploy more capital each year to maintain the same growth rate. That doesn’t mean the strategy stops working, but it does mean sustaining past growth rates becomes mathematically harder.

And that possibility is likely one of the reasons the market now assigns a lower multiple.

AI Could Also Create Opportunities

It’s also worth remembering that AI doesn’t only introduce risks.

Lower development costs could lead to more niche software products being created across specialized industries. Some of those businesses could eventually mature into exactly the kind of stable, mission-critical companies Constellation likes to acquire.

On top of that, many existing subsidiaries could integrate AI features into their current systems. Customers might be perfectly happy adopting AI improvements layered onto software they already trust, rather than replacing entire systems.

That doesn’t mean AI will automatically be a tailwind. Some businesses could face new competition and some niches may evolve faster than expected. But the outcome is likely more nuanced than the simple narrative that AI destroys legacy software.

Could Lower Software Valuations Help Constellation?

Another possibility that receives far less attention is that the recent sell-off in software valuations could actually benefit Constellation.

Over the past several years, private equity firms and venture-backed buyers have aggressively competed for software acquisitions, driving valuations higher across the industry. That made it harder for disciplined buyers like Constellation to find attractive deals.

If software valuations decline, acquisition opportunities may begin appearing at more reasonable prices.

That said, it’s not entirely clear how much this trend applies to the types of companies Constellation buys. Many of the businesses in its portfolio operate in obscure vertical niches that were never heavily affected by the broader SaaS boom in the first place. A software company serving municipal utilities or transit agencies may not have seen the same valuation inflation as venture-backed enterprise SaaS firms.

Still, it’s entirely possible that Constellation could benefit from a cooler software M&A market if it allows the company to acquire assets at lower multiples.

It’s also worth noting that Constellation has never limited itself strictly to one generation of technology. If AI-driven software companies eventually mature into stable, mission-critical platforms with recurring revenue and strong cash flows, there is no obvious reason Constellation could not acquire those businesses in the future as well.

After all, the company’s strategy has always been about buying durable software franchises, not about avoiding new technologies.

Constellation’s Real Advantage May Be Cultural, Not Technological

One of the most common mistakes investors make when analyzing software companies is focusing almost entirely on the technology. It’s easy to assume the company with the best code, the smartest engineers, or the most advanced AI models will eventually win. In many parts of the tech world that assumption is reasonable.

But Constellation Software plays a very different game.

If you ask longtime followers of the company what its real moat is, many won’t point to the software at all. They’ll point to the culture.

A Decentralized Structure

From the beginning, Constellation built an organization designed to acquire and operate hundreds of niche software businesses without forcing them into a giant centralized structure.

Instead of absorbing acquisitions into headquarters and standardizing everything, the company usually allows those businesses to keep running with their existing management teams and local expertise. That decentralized approach allows Constellation to keep scaling without creating the kind of bureaucracy that slows down most large organizations.

A Reputation That Attracts Sellers

Over time the company has also developed a reputation as a very different type of buyer.

Founders who sell to Constellation generally know their businesses won’t be aggressively restructured, flipped to another buyer, or dismantled for short-term gains. In most cases the business continues operating much as it did before, just within Constellation’s broader network.

That reputation quietly creates a deal-sourcing advantage. When founders eventually decide to sell, Constellation is often one of the first buyers they call.

Capital Allocation As An Internal Competition

Culture also shows up in how capital gets allocated internally.

Constellation’s operating groups constantly evaluate acquisition opportunities, and managers effectively compete with each other for capital. Every dollar invested in one deal is a dollar that cannot be invested somewhere else.

Over time that internal competition tends to reward managers who consistently make disciplined investment decisions.

The Real Moat

None of this guarantees success forever. As Constellation grows larger, maintaining the same entrepreneurial culture becomes harder.

But if there is one reason the company has been able to compound capital for so long, it likely comes down to this foundation. Technology changes constantly. Software platforms evolve and industries shift. Organizations that consistently allocate capital well tend to last much longer.

Constellation may not always own the most advanced software in every niche it serves. But it has spent decades building something that may actually be harder to replicate: a culture designed to identify durable software businesses and compound their cash flows for a very long time.

The Takeaway

At the end of the day, the Constellation debate comes down to one question: is the compounding machine still intact?

The market today seems less confident than it used to be. AI fears, concerns about acquisition runway, and leadership transitions have all pushed investors to assign the company a much more cautious valuation than in the past.

But when you step back and look at the underlying business, most of the core ingredients still appear to be in place. Constellation still owns hundreds of niche software businesses that are deeply embedded in their customers’ operations, generating steady recurring cash flows that can be reinvested into new acquisitions.

That doesn’t mean the future will look exactly like the past. As the company grows larger, maintaining the same growth rate becomes harder. But the key difference today is that the valuation no longer assumes perfection.

If Constellation can simply continue compounding its cash flows at a healthy rate (even something closer to mid-teens growth), long-term returns could still be very attractive from today’s levels.

And for now, there is little evidence that the compounding machine has stopped working.

If you enjoy this kind of deep dive, feel free to subscribe to Investor’s Compass. I publish weekly watchlists, long-form company breakdowns, and the occasional idea I think the market may be mispricing. I’m also thinking of potentially writing about a compounder stock every week, especially unknown ones.

Paid subscribers get access to the full archive and deeper research, with more analysis on the way!